Pipe Dreams

Did Canada deliver on the promises of the Trans Mountain Pipeline and what does that mean for the proposed West Coast Pipeline?

On July 2, 2026, Prime Minister Mark Carney and AB Premier Danielle Smith announced federal backing for a new $35B-plus pipeline following the Trans Mountain corridor to Canada’s west coast.

No oil producer has committed to shipping on the line, and Pembina Pipeline, its only named private partner, says it won’t risk its own capital before a future investment decision. Alberta’s Smith has said the taxpayer share of the cost remains “to be negotiated.” It is, in effect, TMX Part Two.

With the original Trans Mountain Expansion now running for over two years, this is the moment to ask: were the promises made about that project kept? And what does the answer mean for a second one?

The Objectives of The Trans Mountain Pipeline Expansion

One can be forgiven for not recalling what was said back in 2015–2019 when the controversy around the TMX was at its peak. I’ve taken a look back and here are the biggest claims proponents of the project were making during that time in no particular order:

Narrowing the price gap between U.S. and Canadian crude — proponents framed improved market access as the fix for this gap.

Oil Production growth — Kinder Morgan promised the expansion would “support Western Canadian crude oil production growth.”

Profitability — implicit in every government defence since 2018/2019 was that TMX would be a self-sustaining, money-making asset.

Jobs — Kinder Morgan’s 802,000 person-years, was publicly repeated as “15,000 jobs” by Trudeau.

Government revenue — in June 2019 after purchasing the line Trudeau claimed $500 million per year in federal corporate tax revenue alone, once the project was completed.

Green-energy reinvestment — again in June 2019 according to Trudeau: “every dollar the federal government earns from this project will be invested in Canada’s clean energy transition,” including any profit from an eventual sale.

Indigenous economic participation — two distinct sub-promises: (a) direct benefit agreements/procurement contracts, and (b) equity ownership for 129 Indigenous groups, announced March 2019.

National unity — Trudeau and others spoke of TMX being important for unifying the country.

Market diversification — proponents promised the expansion would end Canada’s reliance on a single buyer by opening access to Asia-Pacific markets, particularly China.

So now that we have our baseline, how did we do? What does the data show?

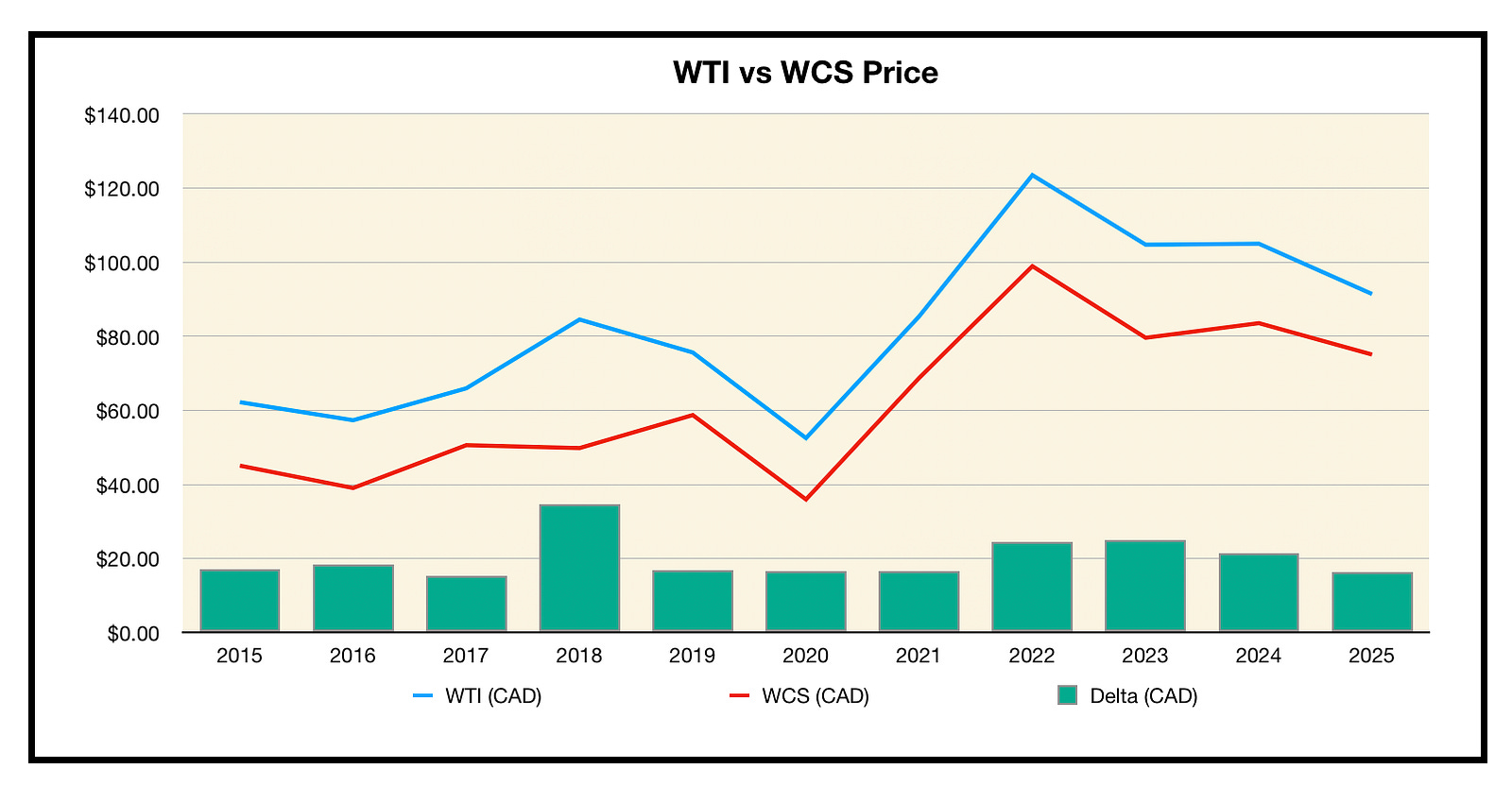

US vs Canadian Oil Price Gap

In 2019, before TMX construction completion or COVID, the average price of a barrel of WTI was $75.62 CAD, and for WCS it was $58.74 CAD, a difference of $16.88. In 2025, after two full years of operations, the average price of a barrel of WTI was $91.40 CAD, and WCS was $75.06 CAD; a differential of $16.34. Almost identical. So on the face of it, this one seems to be a failure.

But oil prices are too volatile and picking a single year is far from a robust methodology. So let’s take the average WTI and WCS price from 2015 to 2023, just before operations of TMX. Once we do that we get WTI at $79.09 and WCS at $58.51, a differential of $20.58. So that means that compared to the 9 year average, 2025 showed about a $4 reduction in the differential. So are we done? It’s a pass? Not quite, and the below chart shows why.

Looking at the delta over the years, it seems to be flat barring a few outlier events. When you take an average of past years you inflate the differential because you include these major events. This error is actually baked into the analysis done by the Canadian Association of Petroleum Producers which claims a $3 USD reduction in the differential. What were these events that swing the differential so high? 2022 was the invasion of Ukraine, 2018 and 2023 however were bottleneck issues; Alberta produced more oil in these two years than they could export by pipeline and rail and this lowered the price of WCS considerably. Why would oil companies knowingly make more oil than they could export? Because oil sands projects take years to plan and build, producers commit to production years in advance based on expected future pipeline capacity, not real-time transport conditions. When that anticipated capacity was delayed, as it repeatedly was, the oil kept coming before the pipeline meant to carry it did.

So in the end, the only thing this pipeline reliably narrowed was the additional differential its own delays helped widen in the first place. There’s a bit of revisionist history happening in discourse at the moment where supporters of TMX argue that the purpose of the line was actually to act as insurance protecting against differential blowouts during rare swing events like 2018, 2022, and 2023, not the everyday price gap. No such distinction was ever made before construction. The argument was always about the flat, day to day differential, not a hedge against occasional crises. This reworking of the objective is pure moving of goalposts after the fact. Even if we consider TMX as insurance against temporary swing events, spending nearly $40 billion to protect $10–20 a barrel during temporary swing events that happen once every 2–4 years, is still questionable. Insurance can sometimes be overpriced.

Final Verdict: Failed

Production growth

Kinder Morgan’s original pitch promised the expansion would “support Western Canadian crude oil production growth” by clearing the transport bottleneck. That mechanism checks out for the years right before completion: Statistics Canada’s own 2023 year in review states producers “ramped up output at the end of the year in preparation for the upcoming completion of the Trans Mountain pipeline expansion,” a claim Alberta’s government backed independently in its own fiscal update. When B.C.‘s November 2021 floods pushed TMX’s completion years behind schedule, producers bridged the gap with crude-by-rail, which nearly doubled to 250,000–300,000 barrels a day by late 2023, according to Canada Energy Regulator data.

This trend continued after completion of TMX as Canada started producing record amounts of crude. A trend directly attributed to pipeline.

Final Verdict: Passed

Profitability

Is Trans Mountain Profitable?

This isn’t really one question, it’s actually two, and conflating them is where most TMX debates go wrong.

Is Trans Mountain Corporation profitable as an operating company?

Did taxpayers recover their investment?

Is TMC profitable, operating basis?

Many people look at this as a simple balance-sheet question. Trans Mountain Corporation’s financials are public record. Revenue exceeds expenses, so it’s profitable. Case closed, right?

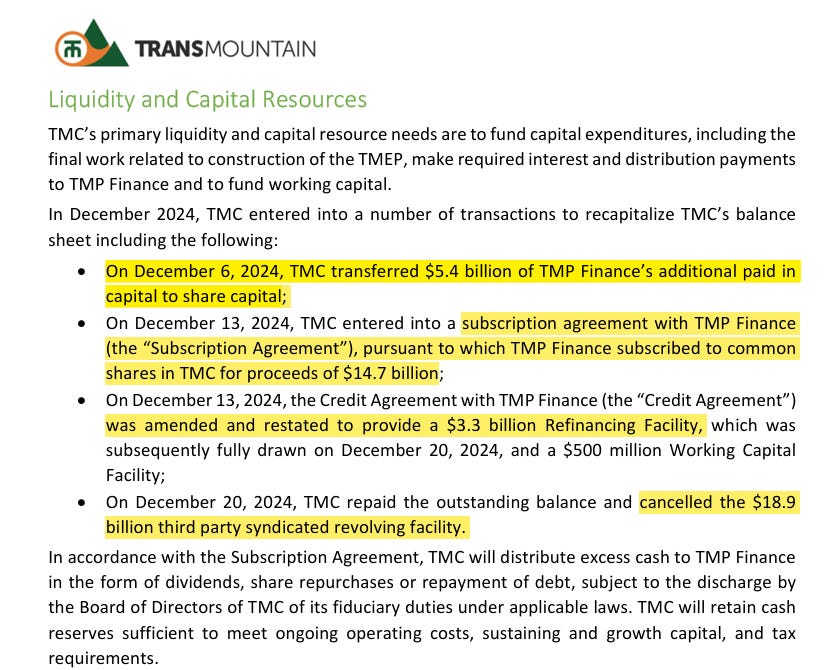

Not exactly. According to its Management Report, TMC carries $12 billion as debt and $23 billion as equity, converted from debt in a single transaction in December 2024. Equity doesn’t generate an interest expense on the books. Debt does.

From TMCs March 2026 Management Report, page 8: “The Facilities have an interest rate of 5% on outstanding amounts, require interest to be paid monthly, and mature on August 31, 2032.” Apply the same 5 percent rate TMC pays on its actual debt to that $23 billion, and the picture flips. TMC’s reported $409 million pretax profit for the first half of 2025 becomes a $167 million loss. A complete reversal.

This matches the independent finding of economist Thomas Gunton, whose calculation of a $166 million loss for the same period was reported by The Tyee. Two independent methods, arriving at the same number. This is the distinction between accounting profit and economic profit: TMX is accounting profitable but likely economically unprofitable once the true cost of all its capital, not just its formally-labeled debt, is recognized.

By converting debt to equity, TMC legally removed the associated interest expense from its own income statement. The move is documented in the company’s own financial notes, buried in a disclosure most readers will never open. Nowhere in TMC’s public communications is this structure explained.

Did taxpayers recover their investment?

TMC has yet to be sold to a private buyer so at the moment the only cash coming into the government is the taxes paid and the revenue from the line. So then let’s ask a separate question: how long until the government recoups its initial investment if it kept ownership? The $4.5 billion to buy the pipeline, plus roughly $34.2 billion to build it, comes to $38.7 billion. The opportunity cost on that sum is enormous. When does it come back? According to their own Q1 2026 report: TMC has already returned $2.2 billion in cash since the expanded system entered service in 2024. Netting that out, $36.5 billion remains outstanding from 2026 onward.

Being generous, let’s assume the pipeline runs completely full from now on. It only hit that mark once, in June 2026, during a Middle East oil crisis its own executives call unpredictable mind you. Scaling last year’s actual cash returns up to full capacity, the government would get about $2 billion a year back.

Against the $36.5 billion to go, simple addition says that money comes back in about 18 more years, around 2044. But raw addition ignores something every economist agrees on: A dollar today is worth more than a dollar promised twenty years from now. If someone offered you $100 today or $100 in ten years, you’d take it today, even with zero inflation. Money now can be invested, spent, or kept safe. Money promised later might not show up at all.

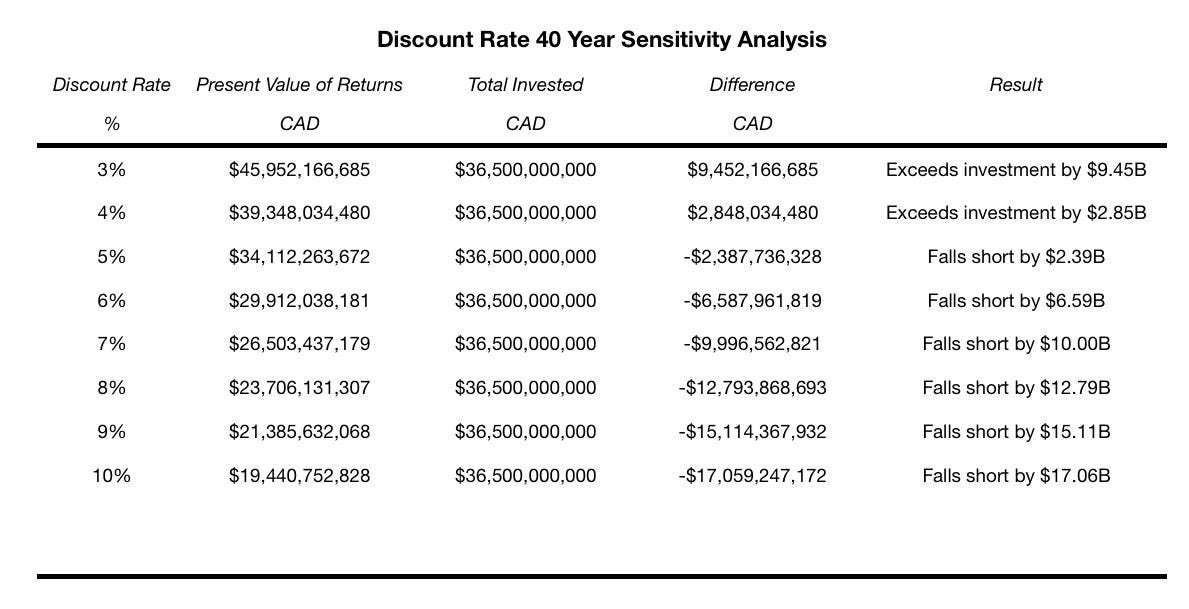

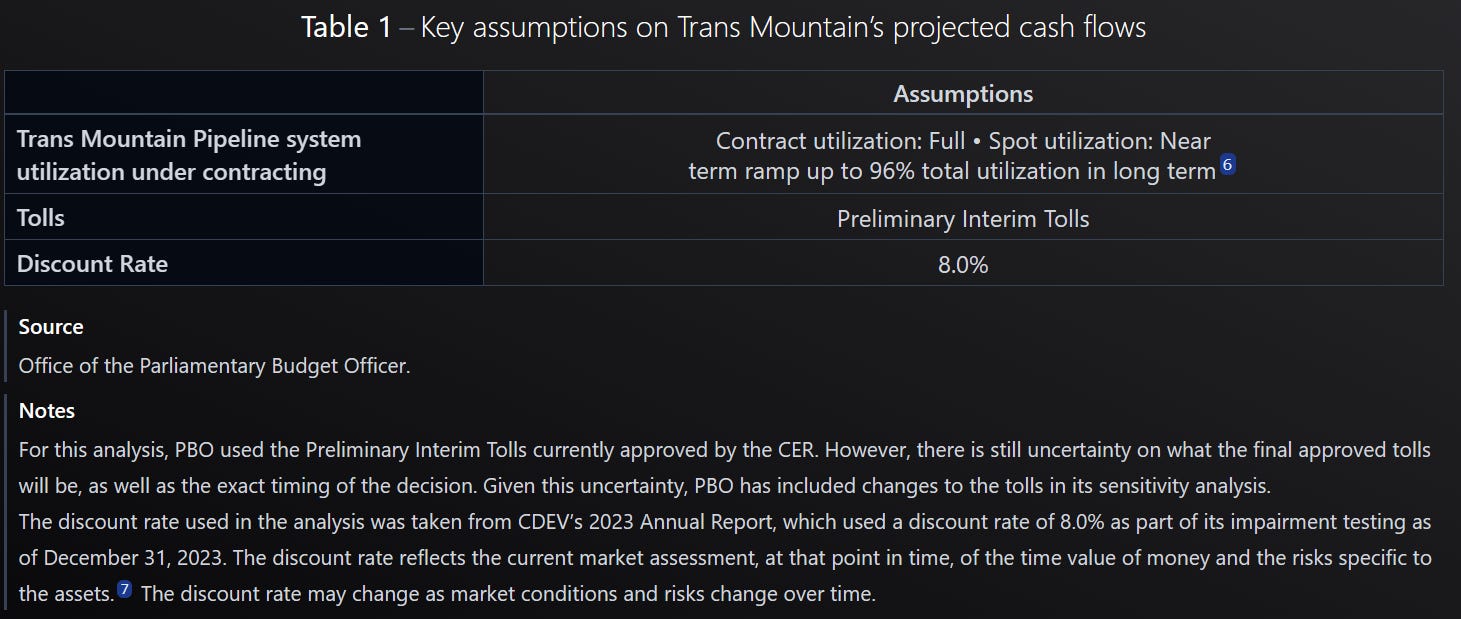

To account for that, you apply a discount rate, and you can’t just pick one out of thin air. Here’s what that same $2 billion annual return implies at different rates, over a 40-year horizon, the same window Canada’s Parliamentary Budget Officer uses in its own official analysis of this pipeline:

The breakeven point sits around 4 percent. At every rate from 4 percent up, over a realistic 40-year window, the investment falls short. I used 8 percent, the exact rate Trans Mountain’s own parent corporation, CDEV, used to test whether its own pipeline assets were worth what they claimed on paper. That is not a rate chosen to make the pipeline look bad (in fact I am being more generous than the PBO by assuming 100% utilization from 2026 onward); it’s the rate its own owner and its own government watchdog already use on themselves. At 8 percent, the shortfall comes to about $12.8B.

Trans Mountain isn’t standing still, though. The company is already spending $3 to $4 billion to add another 300,000 barrels a day of capacity by 2028, on top of the $38.7 billion already sunk. That new capacity is far cheaper per barrel than the original pipeline, at roughly $10,000 to $13,000 a barrel versus $44,000 for the original build.

Stretch every assumption as far as it can honestly go, and nominal payback does improve. But run the same 40-year, 8 percent analysis on the expanded system, and the total comes to $31.70 billion, against $41.7 to $42.7 billion invested. Still short.

A critic will push back saying TMX increased both price and production, and the resulting tax revenue and royalties should count too, not just TMC’s own payments to Ottawa. We showed earlier they’d be wrong about oil prices so let’s address production. CAPP’s own figures show total industry payments to government, including income taxes and royalties, rose from $31.0 billion in 2023 to $32.9 billion in 2024, a $1.9 billion increase, the same year TMX opened. 2024 is used here because it’s the most recent year with a reconciled figure; CAPP’s own 2025 royalty estimates remain incomplete and inconsistent, with a fuller number not expected until the end of this year. With production up in 2025 but prices down over the same period, 2025’s total could end up flat but again we won’t know until numbers are published later this year.

Grant TMX credit for the entire increase, not just its narrow attributable slice, and stack it on top of the pipeline’s own full-capacity cash flow using the pipeline owner’s own 8 percent discount rate, the payback timeline moves from never to year 21, still past the 20-year shipper contract lifespan.

That is the most generous version of the critic’s case this section can construct, and it still describes a multi-decade wait, longer than the contracts signed by the shippers. It also assumes a single year’s tax increase, shaped by multiple factors, holds flat for over two decades, which we all know to be impossible; total industry payments spiked to $45.5 billion in 2022 on the Russian invasion of Ukraine, then fell to $31.0 billion in 2023.

We can always play with a model like this and add assumptions to make almost any outcome appear. I haven’t even mentioned the fact that TMC is in an ongoing dispute with its shippers over tolls which increased above the original agreements made as construction costs ballooned. The outcome of this dispute could result in lower tolls and thus lower revenues. Then again the crisis in the middle east could move things in the other direction for TMC with a prolonged closure of the straight of Hormuz spiking oil prices and thus royalties but this is impossible to model as the situation is actively changing. Currently, only by stacking credit after credit, most of it resting on generosity that the evidence doesn’t support, does a payback even theoretically emerge, and even then it takes longer than the shippers’ own contracts run. Keep that in mind the next time someone tells you the line is making money, or paying back its cost, based on assumptions nobody has bothered to stress-test.

After looking at these numbers in detail one starts to understand why the government hasn’t launched a real sale process but only exploratory talks. PBO’s own valuation, $29.6 to $33.4 billion, sits well below the $38.7 billion actually spent. Selling at PBO’s own number would mean writing off the difference and admitting the loss out loud.

Final Verdict: Failed

Jobs

In November 2016, Prime Minister Justin Trudeau promised the Trans Mountain Expansion would create “15,000 new, middle-class jobs,” with no timeframe specified. The highest independently-reported headcount I was able to find is 13,600, in 2022, per Business in Vancouver. Not quite the 15,000 promised.

The promise didn’t specify construction jobs however and the regional economic boom in the towns along the line is well documented. Acacia Pangilinan, Executive Director of the Kamloops & District Chamber of Commerce, said “there was massive economic spinoff that stayed in the community because we housed the workers.” Edson’s hotels ran full and its population jumped. Valemount and Clearwater felt the boom too. Local officials there were candid that it cut both ways, bringing real economic activity alongside heavier truck traffic and strain on local services.

It’s not hard to imagine that the boom these towns received added jobs to their services and hospitalities industries though I am unable to show that through data publicly available. 1,400 jobs spread across multiple AB and BC towns over multiple years is within the realm of possibility. Knowing about the boom but still calling this a failure because of a less than 10% variation in the promised number would be a dishonest technicality so this one just barely squeaks by with a passing grade.

Final Verdict: Passed

Government Revenue

In June 2019, Trudeau promised “additional corporate income tax revenues from the project alone could generate $500 million per year.” TMC’s own filings show roughly $120 to $125 million a year in federal corporate tax, about a quarter of the promise.

Even reading this promise at its broadest, as all federal corporate income tax from the wider oil sector, the data doesn’t help. CAPP’s own figures show the income tax payments from the industry to the government specifically fell from $7.9 billion in 2023 to $7.7 billion in 2024, the exact year TMX opened.

You’d be correct to remember at this point that while taxes decreased, royalties increased (taxes and royalties are calculated through very different mechanisms) and the combined total rose from $31.0 billion in 2023 to $32.9 billion in 2024. This may lead you to think surely in that $1.9B increase, at least $500M of it was because of TMX. In the profitability example we were generous and credited all of the $1.9B increase to TMX, but how much of it does it really get credit for?

Of the $1.9 billion increase, CAPP’s own attribution work puts TMX’s realistic share at roughly $1.0 to $1.3 billion, using their own $4–5 billion industry-revenue estimate for the differential effect and their own historical ratio of government take to industry revenue. That’s all revenue though, royalties go to the province and federal taxes go to the federal government. So what’s the federal portion of the $1.0 to $1.3 billion? That’d be roughly $246 to $308 million a year. Using CAPP’s own ratio of federal income tax to total government payments it’s still short of the $500 million originally promised.

Final Verdict: Failed

Green Energy Reinvestment

At this point the green energy pledge is a joke. The money that was supposed to fund Canada’s clean energy transition doesn’t exist due to the reasons outlined above, and seven years later, the government is green-lighting another oil pipeline instead.

Final Verdict: Failed

Indigenous economic participation

Direct benefit agreements have been largely delivered. TMC’s own figures, confirmed via Canada.ca in March 2023, showed agreements with 81 Indigenous communities worth over $657 million, generating $4.8 billion in Indigenous-based contracts.

Equity ownership remains unresolved. In March 2019, the federal government promised 129 Indigenous groups the chance to acquire ownership stakes at “zero financial contribution,” with no timeline attached. Seven years on, no stake size was ever finalized, no transaction structure was agreed to, and the promised second phase of divestment was never launched. Ottawa’s only public statement remains that it will happen “in due course,” the same non-answer used in year one. That silence has now outlasted the pipeline’s entire construction timeline.

A sale which includes Indigenous ownership could be announced tomorrow, in which case this becomes an instant pass. Until then, it sits alongside a long history of unfulfilled commitments this country has made to Indigenous people.

Direct Benefit Final Verdict: Passed

Equity Ownership Final Verdict: Fail

National Unity

In July 2019 Trudeau said “We do not have to pit one concern of the country against another” and continued on to say that conservative claims of a threat to national unity were something “we categorically reject.” He again talked about western alienation in October of that same year saying “It’s extremely important government works for all Canadians” while Jason Kenney said “It’s about time Ottawa started working for Alberta.” The Fraser Institute made the case explicitly in a 2019 op-ed titled “Trans Mountain expansion good for all Canadians — and Confederation.”

Seven years later, Alberta has a more vocal and visible separatist movement and a non-binding separation referendum scheduled for October 19, 2026.

One can always say that without TMX things would be worse to which I would genuinely ask how? A growing separatist movement that seems to be well funded and mobilized is nudging the provincial government to hold a referendum when a majority of the province opposes separation. Could someone honestly believe Alberta would have separated by now without TMX? In any case, “it could be worse” is not success.

Final Verdict: Failed

Market diversification

Proponents promised TMX would end Canada’s near-total dependence on the U.S. as a buyer by opening Asia-Pacific markets. China bought an average of just 7,000 barrels a day of Canadian crude in the decade before 2023, according to ship-tracking data reported by Hydrocarbon Processing and Pipeline & Gas Journal.

Since the expansion reached full operations in mid-2024, China has purchased an average of 207,000 barrels a day, overtaking the United States as the single largest buyer on the pipeline. Total Canadian crude exports to non-U.S. destinations rose nearly 60 percent to a record high in 2024, per Statistics Canada, with South Korea, Japan, and India also buying meaningfully more.

Some of this shift is opportunistic rather than purely pipeline-driven, tied to Trump-era tariff threats and China’s own effort to diversify away from Russian and Venezuelan crude. But none of the redirection was physically possible without the added capacity.

Final Verdict: Passed

Conclusion

So, was it worth it? That really depends on what you value as a taxpayer. If you only care about government balance sheets and dollar return on investment or if you hold dear climate efforts and green technology transitions, you have every right to be frustrated.

If you value strategic positioning in Asian markets and diversification of oil customers, it was worth every penny as TMX’s cleanest, long-term, unambiguous win is real. China now buys more oil through this pipeline than the United States does, up from a 7,000 barrel a day afterthought to 207,000 barrels a day in under two years. This may end up a pyrrhic victory however as China’s own state oil company forecasts its total oil demand already peaked in 2025, driven by EV adoption the International Energy Agency calls too fast to ignore. Nearly half of new cars sold in China were already electric in 2024. That share is projected to top 80 percent by 2030, displacing an estimated 2.7 million barrels of oil a day globally by then. The customer TMX was built to chase may need less of what it’s selling with every passing year, not more.

If you value reconciliation, it’s a mixed bag, the temporary benefit during construction to Indigenous groups was indeed real but the equity ownership promise remains unresolved. This week, the same government made it again, for a second pipeline, “a meaningful equity stake reserved for Indigenous Peoples,” without ever settling the first one. This is Ottawa’s Lucy and the football moment. Indigenous communities line up to take the kick, and at the last second, the ball isn’t there. Nobody would call it a coincidence after the second attempt.

The West Coast Pipeline is being sold on identical language to TMX: market access, jobs, government revenue, Indigenous ownership. It carries a weaker commercial foundation than TMX had at the same stage, with no shipper commitments and a private partner unwilling to risk its own capital before a final investment decision. What isn’t in question is the price tag. That’s money that, on TMX’s own evidence, may never come back, at a moment Canada faces real, competing demands for that scale of capital in healthcare and the energy transition. If Trans Mountain is the evidence for how this bet plays out, the record argues for skepticism.

A country’s infrastructure should reflect what its people value most. If we continue to accept paper promises on empty terms, we are defining our national character not by our ambition, but by our willingness to buy into the exact same pipe dream.

Twice.